125-126 / 207

125-126 / 207

125

Industry Overview

MARINE

The marine industry is a dynamic and vibrant marketplace where commerce, passengers, oil & gas, and defense converge in a single global ocean. Today 90% of

the world’s goods are transported over water. Yet uncertainty can dramatically impact the industry without warning, challenging even the most seasoned operators.

Increasing environmental restrictions are also challenging the industry across all segments. For example, requirements to use low sulfur fuels are expected to

cost the industry $50B a year if they go in effect in 2020. Shippers may also be charged a carbon tax. As the marine industry faces ever more stringent cost

competitiveness, vessels need to perform efficiently with reduced fuel consumption, emissions and maintenance levels.

GE powers, propels, positions and predicts the marine industry

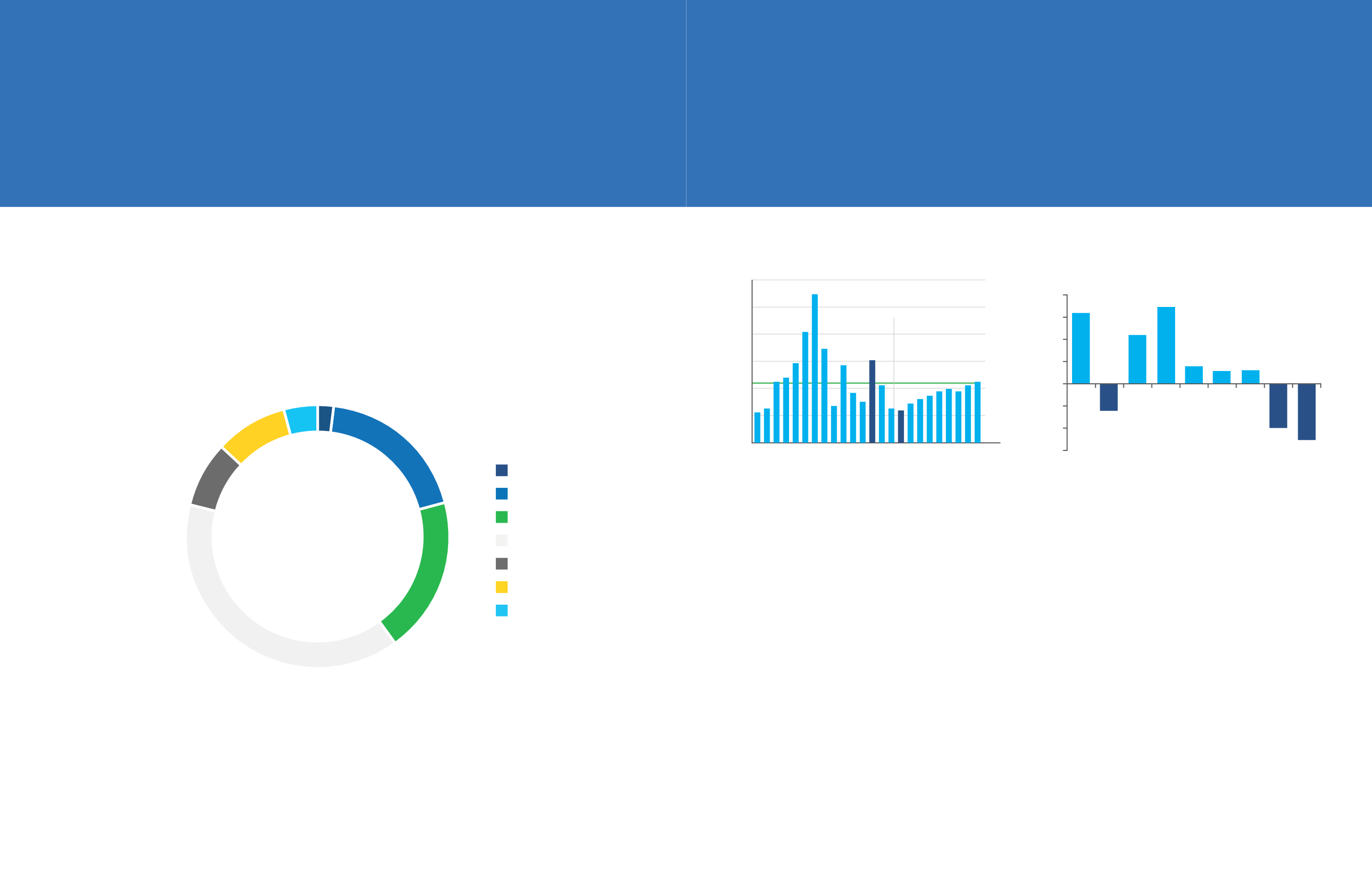

GLOBAL ORDER BOOK BY VESSEL TYPE

90% 4X

7%

OF THE WORLD’S GOODS ARE

TRANSPORTED OVER WATER

TRANSITION TO GAS IS

GROWING AT A PACE 4X THE

RATE OF OIL

ESTIMATED AVERAGE

DOWNTIME ON DRILL

SHIPS IS 7%

FACTS & FIGURES

Passenger

Offshore

Tankers

Bulk carriers

Gas

Containerships

Other cargo

2%

19%

19%

39%

8%

9%

4%

126

Developments in Marine

A CYCLICAL INDUSTRY IN A VOLATILE WORLD

Offshore

Offshore oil & gas operators face their own unique challenges. At $50 per barrel, only ~20% of fields are viable and many big investment decisions, especially

by IOCs, are being delayed. At the same time, energy demand is still growing and many governments have high GDP dependence in offshore oil production. As

exploration moves into deeper and more hazardous environments, operators require sophisticated equipment that enables and provides efficient, safe and

cost effective operations. An over-supply still remains on oil rigs today, so fleet re-deployment will be largely focused on revenue-generating floating production

storage and offloading going forward. Regional growth is shifting from Latin America to Asia, especially China, as government investment has increased in

high-tech “white list” yards.

Merchant

Reducing equipment footprint and weight is key for commercial vessels, while low vibration and noise are primary goals for passenger vessel solutions.

Demand for import and export of goods has constrained the shipping market, but environmental regulations and increase in passenger traffic are both driving

developments and growth in this sector. China cruise passenger growth is expected to grow by 3x by 2020, prompting investment. Incremental regulations are

in place for emissions and energy efficiency. China is capping sulphur emissions in key ports in preparation for its 2020 global limit, which will drive demand for

LNG-capable vessels and hybrids.

Naval

As the world faces tight economic conditions, many government budgets are constrained. As a result, there has been a trend of naval platform restructuring

over the past few years. Targets to reduce total cost of ownership have caused investment to be placed on customized platforms for future capability needs.

Defense systems are large power consumers that must be able to complete a mission. Keeping a low profile that holds up under fire is a must for naval vessels.

Increased power with low noise signatures and high shock resistance are central naval needs. A shift to smaller vessels, more suited to act as a hybrid and

energy efficient solution has occurred. The range of high-tension regions in today’s geo-political climate require flexible, multi-role vessels.

TOTAL SHIPBUILDING INVESTMENT CYCLES PRELIMINARY 2016 EXPLORATION &

PRODUCTION SPENDING DOWN ~25%

6,000

5,000

4,000

3,000

2,000

1,000

0

% 40

30

20

10

0

-10

-20

-30

2001

2003

2005

2007

2009

2008

2009

2010

2011

2012

2013

2014

2015[e]

2016[e]

2011

2013

2015

2017

2019

2021

2023

Total shipbuilding

investment cycles

Preliminary 2016 E&P

spending down ~25%

Led to ~50% ‘14-’15 drop

in project investment

$136B

‘13

History

Forecast

Historical average

$135B

‘25e

$59B

‘16e