107-108 / 207

107-108 / 207

107

Industry Overview

OIL & GAS

GE enables reliable, safe and highly efficient processes across

Oil & Gas operations

The Oil & Gas industry is facing downward commodity price pressures unseen in 30 years. In the second half of 2014, the Oil & Gas industry saw a 40% decline in

the price of oil. This dramatic shift is driving a need for improved efficiency in existing operations to preserve margins and maintain reinvestment rates. Operators

are also challenged with maintaining a reliable supply of power. Situated in sprawling facilities, refineries are especially heavy power users. Expensive electrical

assets run continuous processes involving distillation towers, processing tanks and pumps. Downtime of this equipment costs operators millions per day. The Oil

& Gas industry needs a bold new vision for unlocking hidden value and unprecedented productivity gains from the reservoir to the refinery.

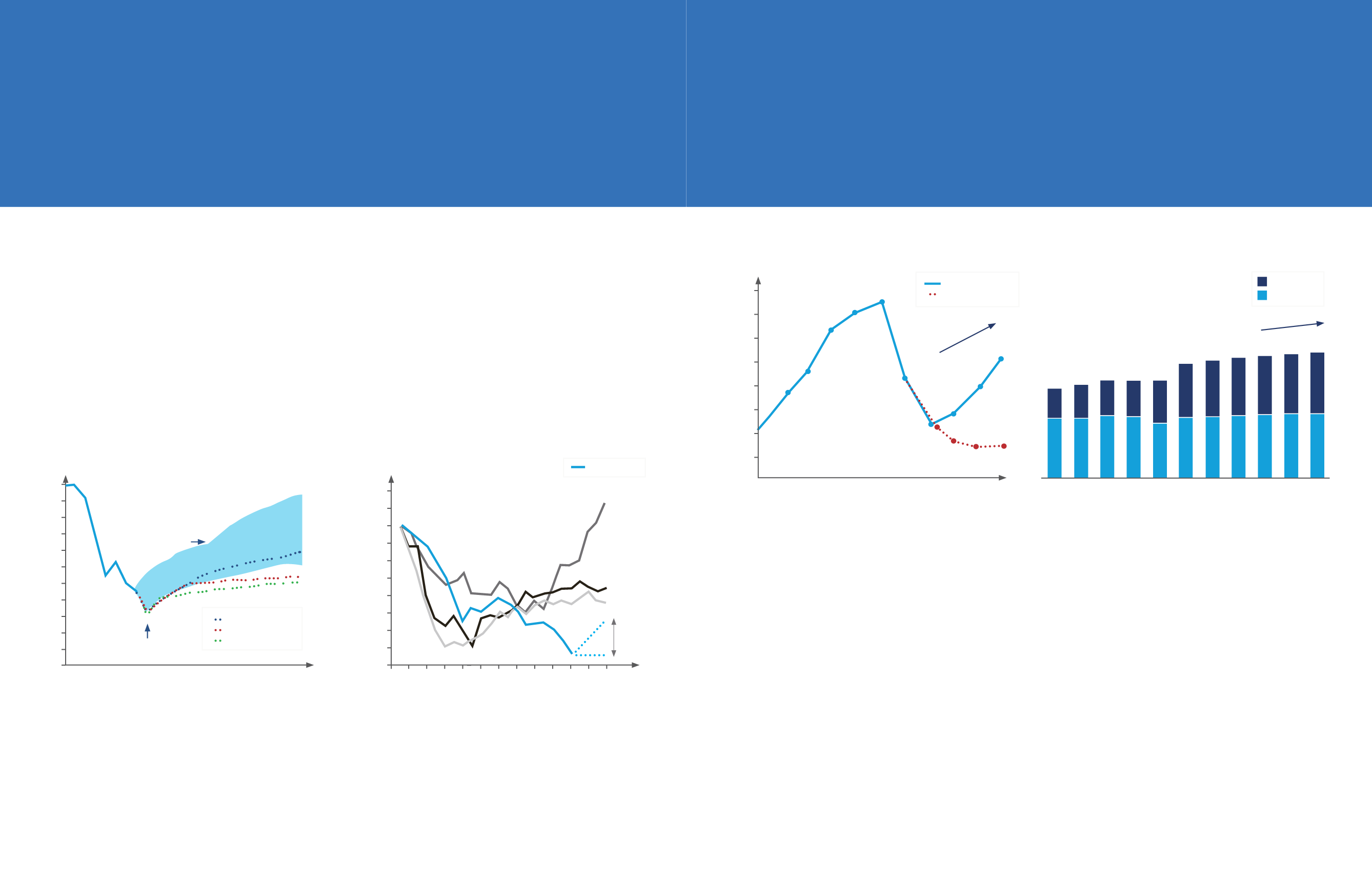

BRENT PRICE PROJECTIONS

PLANNING FOR A WIDE RANGE OF

SCENARIOS

BRENT PRICE AFTER HISTORIC PEAKS

PRICE FALL LONGER THAN PREVIOUS

CYCLES

FACTS & FIGURES

110

100

90

80

70

60

50

40

30

20

10

0

120

110

100

90

80

70

60

50

40

30

20

1Q14

0 2 4 6 8 10 12 14 16 18 20 22 24

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

4Q18

1Q19

2Q19

3Q19

4Q19

$/BBL

(quarterly average)

Brent price

peak = 100

Months of the peak

time

‘97 - ‘00

‘85 - ‘88

‘07 - ‘11

Range of

forecasts

Range of analyst forecasts

Dec ‘15 - Feb ‘16

$26 Jan 20th

‘14 - ‘16 to date

Slow recovery

Sustained Downturn

Futures Mar 24th

1

50% UP TO 10%

DAY OF LNG PRODUCTION LOSS

CAN IMPACT UP TO $5-7M

IN REVENUES PER DAY

OF SKILLED OIL & GAS WORKERS

ARE EXPECTED TO RETIRE IN THE

NEXT 5-7 YEARS

CAPEX REDUCTION THROUGH GE’S

ELECTRICAL AND MECHANICAL

INTEGRATION

108

UPSTREAM CAPEX PROFILE

DOWNSTREAM CAPEX PROFILE

Upstream

With limited resources and funding, oil and gas companies are faced with

a challenging predicament and must determine a way to invest for future

demand in a more deliberate and productive manner. By the end of 2016,

exploration and production (E&P) capex in the upstream space is expected

to be down over 35% since the peak of $673B spend in 2014. Furthermore,

a slow recovery is predicted and a return to 2014 spending levels is not

expected until the next decade. While production and well count are down

globally, the Middle East market has remained resilient with 2017 E&P

expected to increase by 3%. As oil prices begin to recover and grow above

$50 per barrel, onshore shale investment and production in the United States

is expected to rebound. Subsea and Offshore activities, as well as Onshore

activities outside of North America and the Middle East, are anticipated to

face a longer and more challenging recovery cycle as more risky project

funding is delayed or halted altogether.

Midstream & Downstream

Although an imbalance between supply and demand has caused significant

turmoil related to oil prices in recent years, long term demand for oil will

remain. As economic development and urbanization occur, there will

continue to be an ongoing need for efficient distribution of oil to end users.

As a result, the less volatile downstream and pipeline markets are expected

to see continued growth over the coming years. An offset to this effect is

the emergence of alternative energy sources and increased regulation that

support a corresponding need for operational efficiency in downstream and

pipeline technology.

Developments in Oil & Gas

BETTER PROJECT EXECUTION, LOWER COST AND INCREASED PRODUCTIVITY

($B)

($B)

time

Slow recovery

Sustained Downturn

‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19

Petrochems

+2% CAGR

+10% CAGR

Refinery

42

28

14

28

16

29

17

29

17

29

20

29

25

29

26

29

27

30

27

30

28

30

29

44 46 46 46

54 55 56 57 58 59

‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15 ‘16 ‘17 ‘18 ‘19

700

650

600

550

500

450

400

350

404

466

527

614

651

673

510

412

429 381 371 374

556

491

439